Imagine logging into your favorite crypto exchange only to find a black screen where your portfolio used to be. For thousands of traders in Thailand, this wasn't a hypothetical nightmare-it was reality starting in late June 2025. The Thai government pulled the plug on major foreign peer-to-peer (P2P) cryptocurrency platforms, marking one of the most aggressive regulatory shifts in Southeast Asia.

If you are trying to trade Bitcoin or Ethereum from Bangkok today, the rules have changed drastically. You can no longer use global giants like Bybit or OKX if they aren't licensed locally. This guide breaks down exactly what happened, why it happened, and how you can navigate the new landscape without losing money or breaking the law.

The Crackdown Explained

To understand the current situation, we need to look at the timeline. In early 2025, the Thai Securities and Exchange Commission (SEC) is the primary regulator overseeing capital markets and digital assets in Thailand announced emergency decrees targeting unlicensed digital asset businesses. The goal? To stop money laundering and curb online scams that were costing Thai citizens millions.

On April 13, 2025, two Royal Decrees were implemented:

- Royal Decree No. 2 on Digital Asset Businesses: This mandated that any foreign crypto platform targeting Thai users must obtain a license from the Thai SEC.

- Royal Decree No. 2 on Technology Crimes: This gave the Ministry of Digital Economy and Society (MDES) the power to block access to unlicensed platforms immediately, without needing court approval.

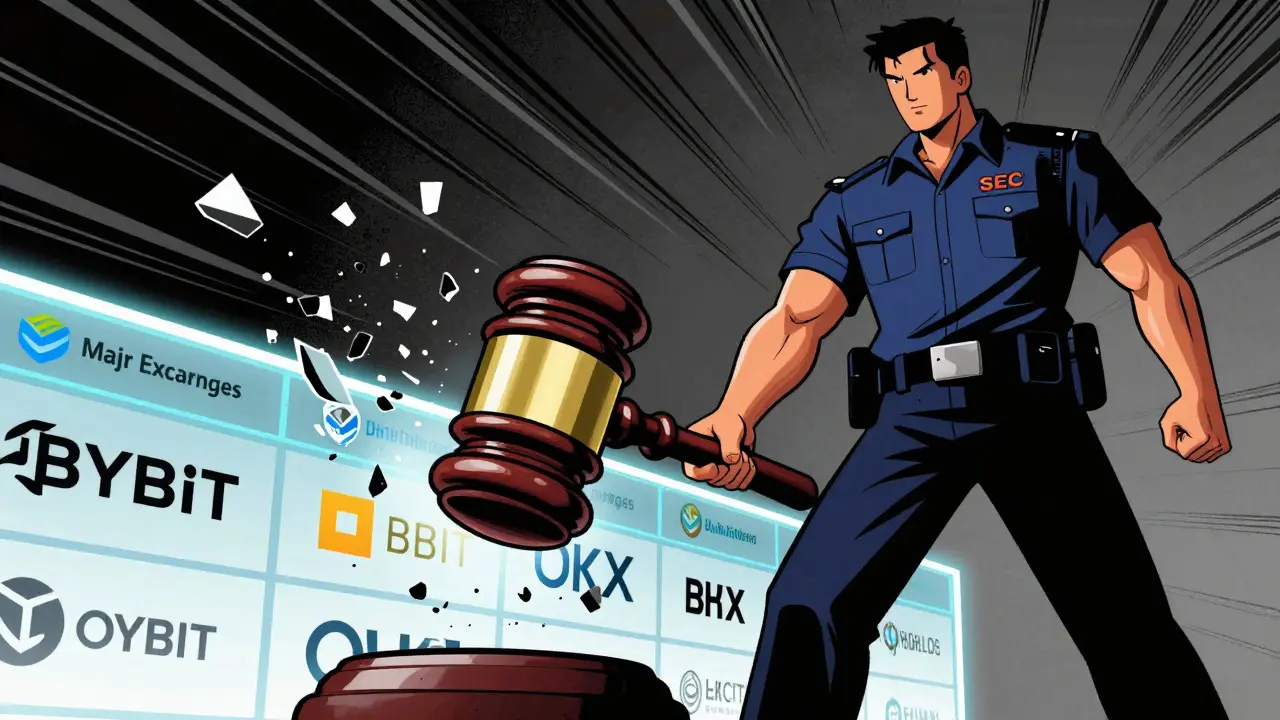

The enforcement date was set for June 28, 2025. On that day, five major exchanges-Bybit, 1000X, CoinEx, OKX, and XT.COM-were blocked nationwide. If you tried to access them after this date, your connection was cut off by local internet service providers.

Who Was Targeted and Why?

You might wonder why these specific platforms were chosen. These weren't small, obscure sites. They were some of the largest players in the Asian crypto market. The SEC argued that these platforms operated illegally under Thailand's Digital Asset Business Act is the legal framework governing the issuance and trading of cryptocurrencies in Thailand. Because they didn't have local licenses, they were considered "unlicensed" regardless of their global reputation.

| Platform Name | Status Before Ban | Reason for Block |

|---|---|---|

| Bybit | Major Global Exchange | No Thai SEC License |

| OKX | Major Global Exchange | No Thai SEC License |

| CoinEx | Popular Asian Exchange | No Thai SEC License |

| 1000X | P2P Trading Platform | No Thai SEC License |

| XT.COM | Crypto Exchange | No Thai SEC License |

The penalties for operating or using these unlicensed platforms are severe. Operators face up to three years in prison and fines of 300,000 baht (roughly $8,700 USD). While the primary target was the operators, users were also warned to withdraw their assets immediately. The SEC provided about one month's notice, which many users felt was insufficient time to move large holdings safely.

Impact on Daily Trading and Cross-Border Payments

The ban didn't just affect individual investors; it disrupted business operations too. Many Thai freelancers and small businesses used P2P platforms to receive payments from overseas clients. Suddenly, those channels were closed.

Here is the catch: all digital asset transactions must now occur on locally licensed platforms. This means if you want to send funds from India to Thailand, you cannot do it directly through a global exchange. You must use a regulated domestic intermediary. This adds layers of complexity:

- Higher Compliance Costs: Businesses must navigate multiple sets of Anti-Money Laundering (AML) and Know Your Customer (KYC) rules.

- Payment Delays: Transactions are more likely to be flagged or blocked if they don't meet strict local criteria.

- Limited Options: With fewer platforms available, liquidity can be thinner, leading to wider spreads and higher fees.

For the average trader, this means less freedom. You can't just hop on a global app and trade whatever you want. You are confined to the walled garden of Thai-regulated exchanges.

What Is Still Legal?

Despite the harsh headlines, cryptocurrency itself is not illegal in Thailand. As of 2026, crypto remains a legal "digital asset," but it is not legal tender. You cannot pay for your coffee with Bitcoin, but you can hold it and trade it-if you do it the right way.

The key difference is licensing. Platforms like Bitkub and SATANG.pro, which obtained licenses from the Thai SEC before the crackdown, continue to operate normally. These local exchanges offer a safer, albeit more limited, environment for trading.

Interestingly, the Thai government is still pushing for innovation within its borders. In May 2025, they announced plans to issue "G Tokens," digital asset tokens backed by government bonds, worth approximately 5 billion baht ($150 million). This shows a dual strategy: crush unregulated foreign competition while promoting state-sanctioned blockchain projects.

How to Protect Yourself Now

If you are in Thailand or planning to trade while visiting, here is what you need to do to stay compliant and secure:

- Use Licensed Exchanges Only: Stick to platforms approved by the Thai SEC. Check the official SEC website for the current list of licensed entities.

- Avoid VPNs for Trading: Trying to bypass the block using a Virtual Private Network (VPN) is risky. Not only does it violate terms of service, but it could also lead to legal scrutiny if authorities trace suspicious activity back to you.

- Verify Counterparties: If you engage in any form of P2P trading on licensed platforms, ensure the other party is verified. Scammers often exploit confusion during regulatory changes.

- Keep Records: Maintain clear records of all transactions. In case of disputes or audits, having proof of legitimate trading activity is crucial.

The community reaction has been mixed. Some users appreciate the clarity and reduced risk of scams. Others criticize the restrictive nature of the ban, arguing that it stifles financial inclusion and limits access to global markets. Social media discussions reveal frustration over the short notice period given to withdraw assets.

Future Outlook

Thailand's approach may serve as a model for other Southeast Asian nations. Countries like Vietnam and Indonesia have shown interest in tightening their own crypto regulations. If Thailand successfully reduces crypto-related crimes without killing innovation, expect to see similar moves regionally.

However, the challenge remains balancing security with accessibility. Will more foreign exchanges apply for Thai licenses? Or will traders simply move to decentralized finance (DeFi) protocols that are harder to block? Only time will tell. For now, the message from Bangkok is clear: play by the rules, or get left out.

Is Bitcoin illegal in Thailand?

No, Bitcoin is not illegal. It is classified as a "digital asset." However, you can only trade it on platforms licensed by the Thai SEC. Using unlicensed foreign exchanges is prohibited.

Which crypto exchanges are banned in Thailand?

As of June 2025, major foreign platforms including Bybit, OKX, CoinEx, 1000X, and XT.COM have been blocked because they lack local licenses. Always check the latest SEC list for updates.

Can I use a VPN to access banned exchanges?

Technically yes, but it is highly discouraged. Bypassing government blocks can violate terms of service and potentially local laws regarding unauthorized access to restricted services. It also exposes you to greater security risks.

What happens if I trade on an unlicensed platform?

While the primary penalties target operators, users risk losing their funds if the platform is shut down or frozen. Additionally, engaging with illegal financial services can lead to account freezes by local banks and potential legal inquiries.

Are there any safe alternatives for Thai traders?

Yes, licensed local exchanges such as Bitkub and SATANG.pro are safe and legal options. They comply with Thai regulations and offer protection against fraud through mandatory KYC and AML procedures.