Iran’s cryptocurrency mining industry is no longer just about electricity bills and cooling rigs. Since January 2025, every miner operating in Iran must sell a portion of their mined cryptocurrency directly to the Central Bank of Iran (CBI). It’s not optional. It’s not a suggestion. It’s the law.

Why the Iranian government is forcing miners to sell

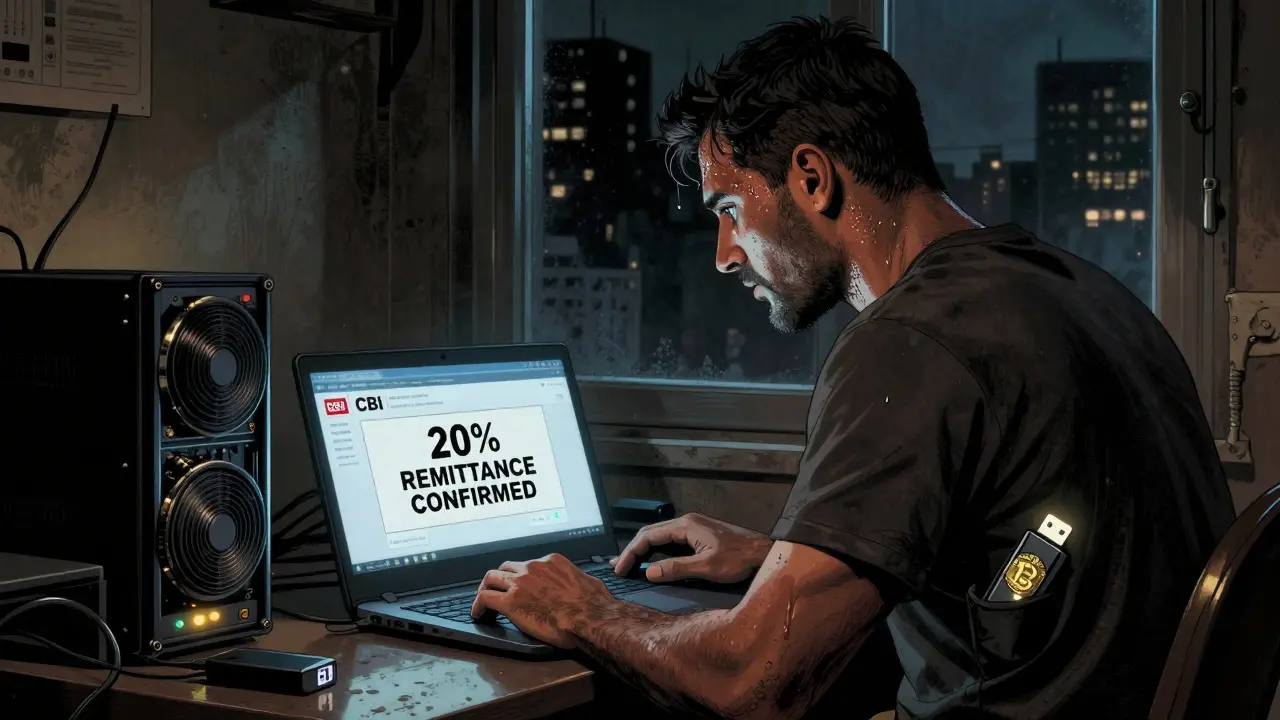

Iran has been mining crypto for years-not because its people love Bitcoin, but because it needs dollars. U.S. sanctions cut off Iran’s access to global banking, so the government turned to crypto mining as a way to earn foreign currency without touching traditional financial systems. But here’s the problem: miners were keeping their coins. They were selling them on black-market exchanges, turning Bitcoin into rials, and pocketing the profit. The government wasn’t getting a cut. In 2025, that changed. The CBI took full control of the crypto sector, demanding that all mining operations register, get licensed, and hand over a percentage of their output. The exact percentage isn’t public, but reports suggest it ranges from 20% to 40% of total production, depending on the size of the operation. Large farms linked to the Islamic Revolutionary Guard Corps (IRGC) are required to surrender even more-up to half their output-to state-controlled vaults. This isn’t just about revenue. It’s about control. By forcing miners to sell to the CBI, the government ensures that every Bitcoin, Ethereum, or USDT entering the country flows through a single, monitored pipeline. The bank then converts these coins into dollars or euros and uses them to import essential goods-medicine, food, industrial parts-that sanctions have made hard to get.How the mandatory sale system works

Miners don’t get to choose where they sell. They’re assigned a CBI-approved digital wallet linked to their registered mining rig. Every time a block is mined, a portion of the reward is automatically transferred to the bank’s wallet. The rest stays with the miner-but only if they’re licensed. Unlicensed miners? They’re out of luck. The government has cracked down hard. In late 2024, rolling blackouts hit cities like Tehran, Isfahan, and Kerman after authorities shut down over 300 illegal mining farms. These weren’t small operations. Some were 100-megawatt facilities hidden in warehouses or inside military bases. The CBI says these farms were using up to 20% of Iran’s total electricity-enough to power entire neighborhoods. Licensed miners, on the other hand, get subsidized power. Electricity costs as little as $0.01 per kWh in some regions. But there’s a catch: the CBI monitors every watt used. If your rig draws more than your licensed capacity, your power gets cut. No warnings. No appeals.Who’s allowed to mine now

Only three types of entities can legally mine in Iran:- State-affiliated entities-mostly IRGC-linked companies with direct access to power grids and security clearance.

- Government-licensed private firms-mostly tech startups that passed strict KYC and AML checks. They must submit daily mining logs, IP addresses of all rigs, and real-time energy consumption data.

- Foreign joint ventures-mostly Chinese firms with partnerships in Iran’s special economic zones. These companies must repatriate 70% of their profits to Iran’s state treasury.

The black market still thrives

Despite the crackdown, crypto trading hasn’t disappeared. In fact, it’s gone underground. On Telegram channels and encrypted apps, Iranians still trade Bitcoin for rials. Prices are higher than official rates-sometimes 30% higher-but people don’t care. The rial lost over 60% of its value in 2024. For many, crypto is the only way to protect savings. The CBI knows this. They’ve tried blocking access to crypto exchanges. They’ve shut down 12 major peer-to-peer platforms. But people keep finding new ways. Some use proxy servers. Others trade in cash through intermediaries. A few even use mining rigs as ATMs-mining a little, selling a little, and keeping the rest. The government’s response? More surveillance. In early 2025, they rolled out a national blockchain monitoring system that tracks all cryptocurrency transactions linked to Iranian IP addresses. If you’re sending Bitcoin to a foreign wallet, the CBI sees it. If you’re mining and not reporting it, they’ll find you.What this means for global crypto markets

Iran is now the 6th largest Bitcoin miner in the world, producing around 4.5% of global hash power. That’s more than Canada and Norway combined. And now, a significant chunk of that output is being funneled into state coffers instead of global exchanges. This has real effects. Fewer Iranian-mined coins are hitting public markets. That means less selling pressure on Bitcoin prices. Analysts at CoinMetrics noticed a 12% drop in daily Bitcoin inflows from Iran in the first quarter of 2025 compared to 2024. It’s not enough to move the market, but it’s enough to matter. Meanwhile, Chinese mining equipment makers are adapting. They’re now selling rigs with built-in CBI compliance modules-software that auto-sends a portion of mined coins to a government wallet. No manual setup. No user control. Just compliance.

The human cost

Behind the numbers are real people. A 28-year-old miner in Mashhad told a local reporter he used to earn $800 a month mining Ethereum. Now, after handing over 30% to the bank, he makes $560. He pays his rent, buys groceries, and still has enough to save a little. But he’s scared. He heard a neighbor got arrested last month for using a second rig without declaring it. Others aren’t so lucky. In Kerman, a group of miners tried to smuggle out 12 Bitcoin in a hidden USB drive. They were caught at the airport. The Bitcoin was confiscated. The men got two years in prison. The CBI says it’s protecting the economy. Critics say it’s creating a digital dictatorship. Either way, Iran has turned mining from a grassroots movement into a state-run extraction program.What’s next for Iran’s crypto policy

The government is now testing a digital rial on Kish Island-a pilot project meant to replace cash and reduce dollar dependence. If it works, they’ll roll it out nationwide. That could mean even tighter control over crypto. Imagine a system where you can’t buy Bitcoin unless you first convert your rials to the digital rial-and the government tracks every step. Some experts think Iran will eventually ban private mining entirely. Others believe they’ll keep the system as-is: state-run extraction with a thin veneer of legality. Either way, one thing is clear: if you’re mining in Iran, you’re not working for yourself. You’re working for the bank.The CBI doesn’t care if you believe in crypto. They care if it earns them dollars. And right now, that’s the only coin that matters.

Jordan Renaud

December 25 2025It's wild how governments turn tech into tools of control. Iran didn't ban crypto-they absorbed it. That's not regulation, that's colonization of the digital frontier. The miners aren't entrepreneurs anymore; they're state laborers with GPUs.

But honestly? If your country's currency is collapsing and you need medicine, what's the alternative? I'd mine too, even if I had to give up half. Survival isn't ideological.

It's a grim reminder that crypto was never just about freedom. Sometimes it's just about staying alive when the system fails you.

And now the Chinese are building compliance into rigs? That's the future. Not decentralization. Not autonomy. Just compliance-as-a-service.

Kinda makes you wonder if we ever really believed in the blockchain revolution, or if we just wanted to get rich while pretending we were rebels.

Luke Steven

December 25 2025Iran’s doing what every desperate state does: monetize chaos.

The CBI didn’t invent crypto mining. They just realized it was the only unblocked pipeline left. Smart move, morally ugly.

Now the real question: when the digital rial rolls out, will they force you to convert your remaining crypto into it? Because that’s the next step. And it’s terrifying.

They’re not trying to stop crypto. They’re trying to own it. And that’s scarier than a ban.

Grace Simmons

December 26 2025This is a textbook case of authoritarian economic adaptation. The Iranian regime is not embracing cryptocurrency-it is weaponizing it. The fact that they are using mined coins to circumvent sanctions while simultaneously crushing individual autonomy reveals the hypocrisy of their entire system.

Western policymakers should take note: crypto is not a libertarian utopia. It is a financial instrument that can be co-opted by any state with sufficient control over infrastructure and surveillance.

This is not innovation. It is extraction dressed in blockchain.

Vyas Koduvayur

December 26 2025Let me break this down for you guys who think this is just about money. Iran’s entire economy is a house of cards built on oil and lies. When sanctions hit, they didn’t have access to SWIFT or dollars or anything. So they turned to mining because it’s the only way to get USD without the IMF breathing down their necks.

But here’s the kicker-the IRGC doesn’t mine for the people. They mine for themselves. The 50% they take from big farms? That’s not for medicine. That’s for drones and missiles.

And the black market? It’s not just about savings. It’s about rebellion. People are using crypto to opt out of the state’s entire economic fraud. The CBI knows this. That’s why they’re tracking every IP, every transaction, every watt.

And now Chinese rigs have built-in compliance modules? That’s the death of decentralization. You don’t own your coins anymore. The state owns them. And you’re just the hardware.

Meanwhile, in the US, we’re still arguing about ETFs. Pathetic.

Jacob Lawrenson

December 27 2025Man, this is the most real thing I’ve read all week. 😅

People act like crypto is some magic freedom coin. Nah. In Iran, it’s a lifeline. And the government didn’t kill it-they turned it into a tax collector with a GPU.

Imagine being a miner and knowing that every time you solve a block, 30% of your reward goes straight to the bank. No choice. No debate.

But honestly? I get it. If my country’s currency was worth nothing and I could mine to buy insulin for my kid? I’d do it too.

Just… doesn’t feel like freedom anymore. Feels like survival with a ledger.

Vijay n

December 29 2025So what you're saying is the government is stealing from miners? Wow what a surprise. But wait they are doing it for the people right? For medicine? Lol. The IRGC is not buying insulin they are buying missiles. And the black market is thriving because people are not stupid. They know the state is lying. And now they are tracking every transaction? What next? Blockchain ID cards? Mandatory wallet registration? This is not crypto this is surveillance with a blockchain logo. And the chinese are making compliant rigs? They are not helping they are enabling tyranny. This is the future of crypto. Not freedom. Control. And we are all just spectators watching the last gasp of decentralization. No one is talking about this. But I am. Because someone has to.

Collin Crawford

December 30 2025Let’s be clear: Iran is not regulating mining. It is nationalizing it under the guise of economic necessity. The fact that private miners are being forced into compliance while IRGC-affiliated entities receive preferential power access is not policy-it’s cronyism. The CBI’s blockchain monitoring system is a surveillance infrastructure masquerading as financial oversight. This is not a model for the world. It is a warning. If you believe in decentralization, you must oppose this. Not because you hate Iran. But because you believe in the principle that no entity-state or otherwise-should have unilateral control over your digital assets. The Chinese compliance modules are the logical endpoint of this trend. You don’t own your coins. The state does. And if you’re okay with that, you never understood crypto to begin with.

Jayakanth Kesan

December 30 2025I think it’s kind of beautiful in a sad way. People in Iran are mining because they have to. Not for profit. Not for ideology. Just to survive. The system broke, and they found a way to keep the lights on.

Yeah, the government took a cut. But at least they didn’t shut it all down. They didn’t arrest everyone. They made a deal: mine, but share.

It’s not perfect. But it’s real. And sometimes real is better than ideal.

Maybe the future isn’t about decentralization. Maybe it’s about shared responsibility-even if the state is the one holding the scales.

Megan O'Brien

December 31 2025So the CBI is effectively acting as a sovereign wealth fund for crypto arbitrage? That’s not policy-that’s rent-seeking with a blockchain veneer. The marginal utility of each mined BTC is being internalized by the state while externalizing the computational and environmental costs onto the populace. The subsidy structure is a classic distortionary incentive, and the surveillance apparatus is a textbook case of digital paternalism. The Chinese OEMs integrating compliance modules? That’s not innovation. That’s commodification of coercion. The entire model is a zero-sum extraction protocol disguised as economic pragmatism. We’re witnessing the necrosis of libertarian crypto ideals in real time.

Kevin Karpiak

January 1 2026Iran is not a victim. It’s a predator. Using crypto to bypass sanctions is illegal under international law. The fact that they’re forcing miners to hand over coins doesn’t make them victims-it makes them criminals with better tech. The black market? That’s the result of their own choices. They broke the rules. Now they’re trying to control the fallout. No sympathy. No exceptions. This is what happens when you build an economy on lies and bombs.

Zavier McGuire

January 2 2026people are getting arrested for smuggling bitcoin in usb drives bro

like what even is this anymore

they turned mining into a prison job

and we still talk about decentralization like its a thing

rip

Janet Combs

January 3 2026I just keep thinking about that guy in Mashhad making $560 now instead of $800.

He’s not a rebel. He’s not a tech bro. He’s just a guy trying to pay rent.

And now he’s scared because his neighbor got jailed for having an extra rig.

That’s not capitalism. That’s not crypto. That’s just… life.

I don’t know what to feel.

Maybe we all thought this was about freedom.

But for him? It’s just about not starving.

Radha Reddy

January 4 2026As someone from India, I see parallels in how governments respond to disruptive technology. The desire to control is universal. But what stands out in Iran is the precision of the control-not brute force, but calibrated extraction.

They didn’t ban mining. They made it part of the state’s financial architecture. That’s sophisticated. And terrifying.

It’s not about ideology. It’s about survival. And in that sense, it’s deeply human-even if the system is not.

Shubham Singh

January 6 2026How quaint. The Iranian state has finally figured out that crypto isn't a currency-it's a revenue stream. And they're extracting it like oil. How original. The IRGC mining farms with subsidized power? Of course. Who else would have the infrastructure? The 'private' miners are just rent-seeking intermediaries. And the Chinese compliance modules? A perfect example of how capitalism serves authoritarianism. The real tragedy? We thought blockchain meant liberation. Instead, it just gave tyrants a better spreadsheet.