Imagine logging into your favorite trading app one morning to find a blank screen. Your funds are inaccessible, the website is blocked by Indian internet service providers, and customer support has gone silent. For thousands of Indian cryptocurrency traders, this wasn't a hypothetical nightmare-it was reality during the massive regulatory crackdowns led by the Financial Intelligence Unit-India (FIU-IND).

If you are wondering which platforms are off-limits and why, the answer lies not in a blanket ban on cryptocurrency itself, but in strict adherence to anti-money laundering laws. As of early 2026, the landscape has shifted dramatically. Cryptocurrency trading remains legal in India, but only through exchanges that have registered with the FIU-IND. Any platform operating without this registration is effectively banned for Indian users, facing website blocks, banking restrictions, and severe legal penalties.

The Core Rule: FIU-IND Registration Is Mandatory

To understand what is banned, you first need to understand what makes an exchange legal. The central entity governing this space is Financial Intelligence Unit-India (FIU-IND), the national agency responsible for receiving, processing, analyzing, and disseminating information relating to suspected financial transactions.

Under Section 12 of the Prevention of Money Laundering Act (PMLA), Virtual Asset Service Providers (VASPs)-which includes crypto exchanges-must register with the FIU-IND. This is not optional. It is the single most important factor determining whether an exchange can operate in India.

Here is how it works in practice:

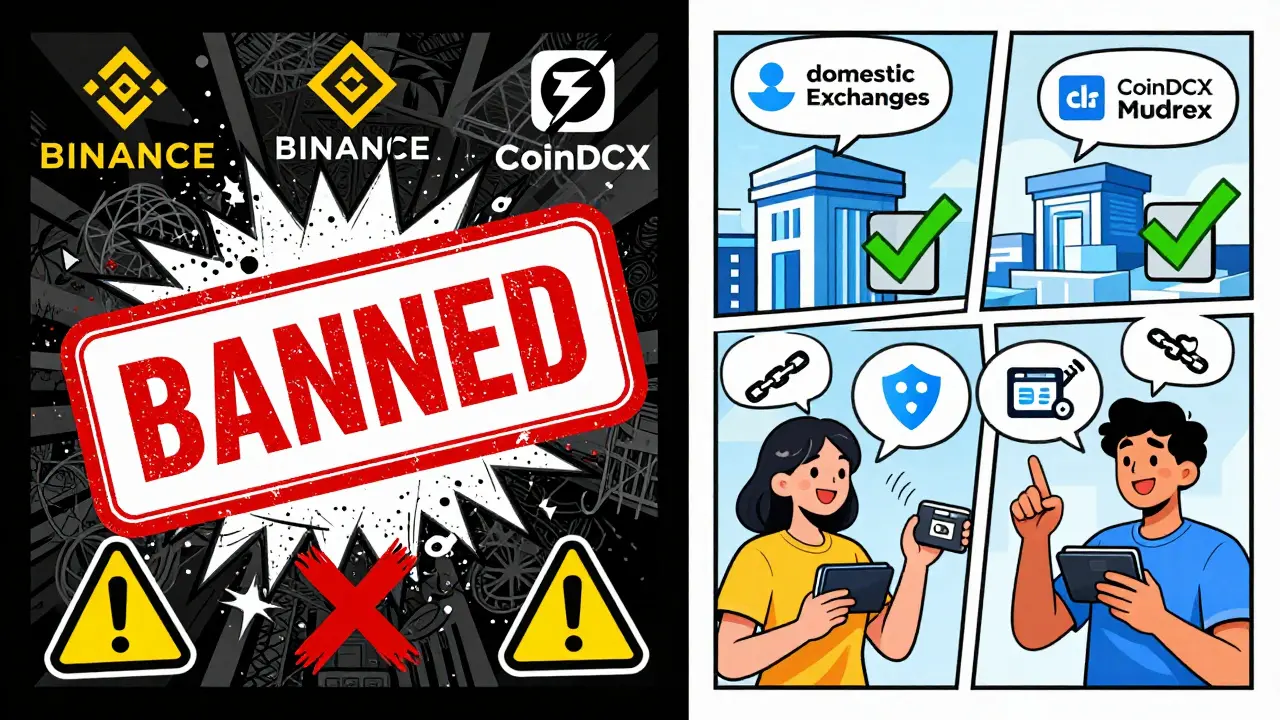

- Compliant Exchanges: Platforms like CoinDCX, a leading Indian cryptocurrency exchange that secured early FIU-IND registration and WazirX, an Indian crypto exchange owned by WazirX Technologies Private Limited are fully operational. They can process INR deposits via banks, offer customer support within Indian jurisdiction, and report transaction data to authorities.

- Non-Compliant/Banned Exchanges: International giants that failed to register or were deemed non-compliant face immediate blocking. Their websites become inaccessible via Indian IPs, and their apps are removed from local app stores.

The distinction is critical. The government did not ban Bitcoin or Ethereum. They banned the *gateways* that do not follow Indian financial surveillance rules.

Which Major Exchanges Were Blocked?

The crackdown accelerated significantly in late 2023 and continued through 2024 and 2025. Several high-profile international exchanges found themselves on the wrong side of the law. Here are the key players affected:

| Exchange Name | Status in India | Reason for Action |

|---|---|---|

| Binance, world's largest cryptocurrency exchange by volume | Banned / Restricted | Failed initial FIU registration deadlines; faced significant penalties and website blocking before attempting re-entry. |

| Bybit, global cryptocurrency derivatives exchange | Banned / Restricted | Lacked FIU-IND registration; paid millions in fines to resolve compliance issues. |

| KuCoin, international cryptocurrency exchange based in Seychelles | Blocked | Website blocked by Indian ISPs due to non-compliance with PMLA requirements. |

| CoinDCX | Legal & Compliant | One of the first domestic exchanges to secure FIU-IND registration. |

| Mudrex | Legal & Compliant | Registered FIU-IND compliant platform focusing on mutual fund-style crypto products. |

Note that while some international platforms like Binance have attempted to return by seeking registration, the process is rigorous. Until an exchange explicitly confirms its active FIU-IND registration status, Indian users should assume it is banned and risky to use.

The Ripple Effect: User Migration and Market Shift

When the bans hit, they didn't just close websites-they triggered the largest migration of crypto users in India's history. Traders who previously relied on global liquidity pools had nowhere to go but home.

Domestic platforms saw explosive growth. CoinDCX reported deposit growth exceeding 2,000% as users fled banned platforms. Similarly, Mudrex onboarded over 10,000 new users within weeks of the major blockades. Other platforms like ZebPay and Unocoin also benefited from this shift.

This migration wasn't just about necessity; it changed market dynamics. Domestic exchanges now hold the majority of retail trading volume in India. However, this came with trade-offs. Users often complained about lower liquidity, higher spreads, and fewer altcoin options compared to the global giants they left behind. Yet, the security of having a regulated entity meant many accepted these compromises.

Risks of Using Non-Compliant Exchanges

You might be tempted to bypass blocks using VPNs or peer-to-peer (P2P) transfers to access banned exchanges like Binance or KuCoin. Before you do, consider the severe risks involved.

- Frozen Assets: If an exchange is banned, there is no guarantee you can withdraw your funds. We have seen cases where users lost access to their entire portfolios because the platform could not process withdrawals to Indian bank accounts.

- No Legal Recourse: If a non-compliant exchange gets hacked or goes bankrupt, Indian authorities will not help you recover your losses. You are outside the protection of Indian consumer laws.

- Tax Nightmares: Compliant exchanges provide detailed transaction reports aligned with Indian tax laws. Non-compliant platforms often lack these features. Under current rules, you must calculate your own capital gains. If you fail to report accurately, the penalty can reach up to 60% under Section 158BA(7) of the Income Tax Act.

- Banking Blacklists: Indian banks monitor transactions closely. Sending money to a known non-compliant exchange can lead to your bank account being frozen or flagged for investigation by the Enforcement Directorate (ED).

The convenience of a familiar interface is rarely worth the risk of losing your life savings or facing legal scrutiny.

Taxation and Data Privacy: What You Need to Know

Trading crypto in India comes with a heavy tax burden, regardless of which compliant exchange you use. As of 2026, the tax structure remains stringent:

- Flat Tax Rate: A 30% tax on all crypto gains, plus a 4% health and education cess, totaling 31.2%.

- No Set-offs: You cannot offset losses from one crypto trade against profits from another. Each transaction is taxed independently.

- TDS (Tax Deducted at Source): A 1% TDS is deducted on every transaction above a certain threshold. This affects your cash flow and requires careful reconciliation when filing returns.

Data privacy is another concern. FIU-registered exchanges are required to maintain user records for up to six years. While this ensures transparency for tax purposes, it means your trading history is permanently accessible to government authorities. There is no anonymity in compliant Indian crypto trading.

How to Verify if an Exchange is Safe

Before depositing any money, take these steps to verify an exchange's status:

- Check the FIU-IND Website: Visit the official FIU-IND portal and look for the list of registered VASPs. If the exchange is not on the list, do not use it.

- Look for INR Banking Partnerships: Legitimate exchanges partner with major Indian banks (like HDFC, ICICI, or SBI) for seamless deposits. If you have to rely solely on obscure third-party payment gateways, proceed with caution.

- Read Recent News: Regulatory statuses change. Search for "[Exchange Name] FIU registration 2026" to see if there are recent updates or warnings.

- Avoid "Too Good to Be True" Bonuses: Some shady platforms offer excessive sign-up bonuses to attract users from banned exchanges. These are often scams designed to steal funds.

The Future of Crypto Regulation in India

The regulatory framework is still evolving. The Finance Bill changes introduced in February 2025 under Section 285BAA mandated stricter record-keeping, with retrospective implications for some registrants. This signals that the government intends to tighten oversight further, not loosen it.

While there is talk of a potential Digital Rupee (CBDC) expanding, private cryptocurrencies remain in a grey area legally, though practically tolerated if traded on compliant platforms. Expect more clarity in 2026 regarding long-term holding taxes and institutional participation, but for now, compliance is king.

For the average trader, the message is clear: Stay within the boundaries of FIU-registered platforms. The era of wild west crypto trading in India is over. Safety, legality, and tax compliance are no longer optional-they are the price of admission.

Is cryptocurrency completely banned in India?

No, cryptocurrency itself is not banned in India. You can legally buy, sell, and hold digital assets like Bitcoin and Ethereum. However, you must do so through exchanges that are registered with the Financial Intelligence Unit-India (FIU-IND). Trading on non-compliant or banned exchanges is illegal and carries significant risks.

Can I use Binance in India in 2026?

As of early 2026, Binance faces significant restrictions in India due to past non-compliance with FIU-IND regulations. While the company has attempted to seek registration, Indian users should exercise extreme caution. Unless Binance explicitly confirms its active FIU-IND registration status on the official FIU portal, it is considered non-compliant and risky to use. Many Indian users have migrated to domestic alternatives like CoinDCX.

What happens if I trade on a banned exchange?

Trading on a banned exchange exposes you to multiple risks. Your funds may become inaccessible if the exchange is blocked or shuts down. You have no legal recourse in case of fraud or hacking. Additionally, you may face difficulties withdrawing funds to Indian bank accounts, and your bank account could be frozen by authorities for linking to non-compliant entities. You also bear the full burden of calculating and paying taxes without assistance from the exchange.

Which crypto exchanges are legal in India?

Legal crypto exchanges in India are those registered with the FIU-IND. Prominent compliant platforms include CoinDCX, WazirX, Mudrex, ZebPay, and Unocoin. Always verify the current registration status on the official FIU-IND website before trading, as this list can change.

How much tax do I pay on crypto profits in India?

India imposes a flat 30% tax on all cryptocurrency gains, plus a 4% health and education cess, making the total effective tax rate 31.2%. There are no set-offs allowed for losses, meaning each profitable transaction is taxed individually. Additionally, a 1% Tax Deducted at Source (TDS) applies to transactions above specific thresholds.

Bronwen Butler

May 23 2026you really think the government cares about money laundering when they are the ones printing worthless paper? its just another way to control us and steal our data

the whole FIU thing is a sham designed to crush innovation while bureaucrats get fat

beti macedo

May 25 2026I must say that this article provides very valuable insights into the current regulatory landscape in India. It is indeed crucial for every citizen to understand the importance of compliance with financial regulations to ensure the stability of the economy.

The migration towards domestic platforms like CoinDCX and Mudrex seems to be a positive step towards a more secure and transparent crypto ecosystem. I hope that all traders will adhere to these guidelines strictly to avoid any legal complications in the future.

Matt Davis

May 27 2026This is absolute bollocks! The Indian government has always been hostile to anything it cannot tax or control, and now they have finally found a way to strangle the crypto market completely under the guise of 'security'.

Do you honestly believe that CoinDCX is any safer than Binance? They are all in the same boat, just some have better lawyers. The liquidity on these domestic exchanges is pathetic compared to what we had before. People are losing money on spreads alone because the market makers have fled.

It is a disaster for retail investors who wanted fair access to global markets. Now we are forced to use inferior local products with higher fees and worse tech support. Typical bureaucratic overreach that destroys value instead of creating it.

Pauline Larocco71

May 28 2026i can totally relate to the fear of losing access to funds its so scary thinking about your savings being frozen overnight

it makes me sad that people have to choose between safety and having good options i hope everyone finds a platform that feels right for them even if it means dealing with higher taxes

Michelle Bonahoom

May 29 2026india needs to stop relying on foreign scams and build its own infrastructure these american companies only care about profits not our security

good riddance to binance and kucoin they were never safe anyway

Ankush Pokarana

May 31 2026one must consider the deeper philosophical implications of state surveillance in digital finance

while compliance ensures order it also erodes the fundamental privacy rights that individuals once held dear in the early days of cryptocurrency adoption

the trade-off between security and liberty is a delicate balance that society must navigate carefully as we move forward into an era where every transaction is recorded and analyzed by governmental entities

perhaps the true cost of this regulation is not measured in rupees but in the loss of individual autonomy and trust in decentralized systems which were originally designed to empower the user rather than subject them to centralized authority

Bianca Vilas Boas Lourenço

June 1 2026oh wow another government telling us what we can do with our own money 🙄

like anyone actually trusts these domestic exchanges after seeing how easily banks freeze accounts for no reason 😒

i guess we should all just sit back and smile while they take 31% of our profits and spy on our every move 🤡

Yash Lodha

June 2 2026have you considered that the FIU-IND registration list is merely a facade for a larger surveillance apparatus?

the data collected from these compliant exchanges is likely being shared with international intelligence agencies under secret agreements that the public is unaware of

your trading history is not just for tax purposes it is being used to build psychological profiles of citizens to predict dissent and suppress opposition before it even begins

the blocking of foreign exchanges is not about money laundering it is about controlling the narrative and ensuring that all financial flows pass through nodes that the state can monitor and manipulate at will

wake up sheeple the game is rigged from the start

Jesse Alston

June 4 2026Hey there! 👋 Just wanted to add a quick tip for anyone feeling overwhelmed by the new rules.

Always double-check the official FIU website directly instead of relying on third-party lists because those can get outdated quickly 🔍

Also keep screenshots of your transactions just in case you need to prove compliance later on 📸

Stay safe out there and don't let the stress get to you 💪

Sarah C

June 5 2026I appreciate the detailed breakdown of the risks involved with non-compliant exchanges. It really helps to clarify why the shift to domestic platforms was necessary for long-term stability.

It might be challenging for some users to adapt to the lower liquidity initially but I believe that patience and careful planning will lead to better outcomes in the end.

Kimberly Herbstritt

June 6 2026Actually I think people are overreacting to the bans

if you cant handle a little regulation then maybe crypto isn't for you

plus the domestic exchanges are getting better every day so whats the big deal

Sharada Vakkund

June 6 2026Let's come together and support each other during this transition period!

We can share tips on how to maximize our gains despite the higher taxes and help newcomers understand the new compliance requirements

No one should feel left behind in this evolving landscape so please reach out if you have questions or need guidance

Together we can make the Indian crypto community stronger and more resilient!

Sudarshan Anbazhagan

June 8 2026it is imperative that one understands the gravity of the situation at hand

the failure to register with the FIU-IND is not merely a technicality but a fundamental breach of the legal framework established to protect the integrity of the national financial system

those who continue to operate outside these boundaries are not only risking their own assets but also undermining the efforts of legitimate businesses that strive to comply with the law

we must demand stricter enforcement and harsher penalties for violators to ensure that the rule of law is upheld without exception

John Gonzalez Bentham

June 8 2026this is all fake news the real reason is to kill competition from indian startups that could challenge the global giants

they want to keep us dependent on foreign tech while pretending to protect us

dont believe the hype

Ellie Riddell

June 8 2026how quaint that we think a database entry saves us from chaos

the irony is thick enough to cut with a knife

we traded freedom for a badge of compliance and now wonder why everything feels so sterile and controlled

but sure lets pretend this is progress

Destiny Kilby

June 8 2026I understand the concerns regarding data privacy but it is important to remember that these measures are in place to prevent illegal activities

without proper oversight the entire system could collapse under the weight of fraud and manipulation

we must accept certain sacrifices for the greater good of maintaining a stable financial environment

Jerry CUNNINGHAM SR

June 9 2026It is essential that we approach this topic with respect and open-mindedness.

While opinions may differ on the efficacy of the regulations it is clear that the intention is to create a safer environment for all participants.

We should encourage dialogue and education rather than division and fear.

By working together we can ensure that the benefits of cryptocurrency are accessible to everyone in a responsible manner.

Shelby Cantu

June 10 2026Stay focused on the facts.

Check the FIU list.

Use compliant exchanges.

Avoid scams.